")

CoreLogic’s latest Single-Family Rent Index (SFRI), which analyzes single-family rent (SFR) price changes nationally and across major metropolitan areas, has found consistent evidence of an SFR market cool down following nearly two years of above-trend rental price hikes.

CoreLogic’s latest Single-Family Rent Index (SFRI), which analyzes single-family rent (SFR) price changes nationally and across major metropolitan areas, has found consistent evidence of an SFR market cool down following nearly two years of above-trend rental price hikes.“Annual single-family rent growth decelerated for the fifth consecutive month in September, but remained at more than twice the pre-pandemic growth rate,” said Molly Boesel, Principal Economist at CoreLogic. “High mortgage interest rates may be causing potential homebuyers to hit pause and remain renters, keeping pressure on rent prices. However, the monthly rent change was negative in September, resuming the typical seasonal pattern for the first time since 2019, which could signal the beginning of rent price growth normalization.”

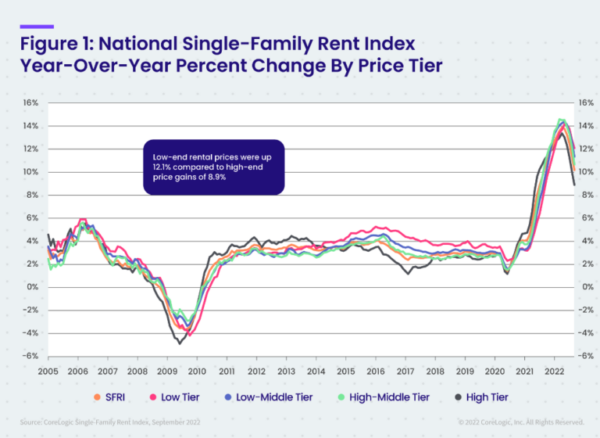

In determining the SFRI, CoreLogic examined four tiers of rental prices. National single-family rent growth across the four tiers, and the year-over-year changes, were as follows:

- Lower-priced (75% or less than the regional median): 12.1%, up from 8.5% in September 2021

- Lower-middle priced (75% to 100% of the regional median): 11.3%, up from 9.4% in September 2021

- Higher-middle priced (100% to 125% of the regional median): 10.7%, up from 10.6% in September 2021

- Higher-priced (125% or more than the regional median): 8.9%, down from 11.1% in September 2021

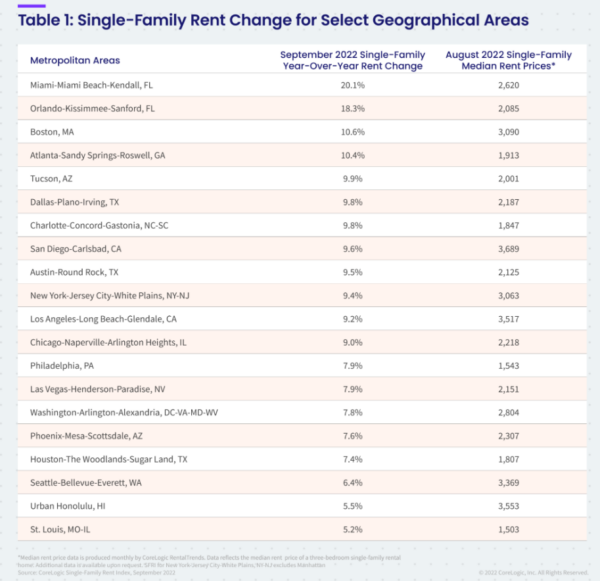

Of the 20 metro areas examined by CoreLogic, Miami posted the highest year-over-year increase in SFR in September 2022 at 20.1%. Orlando, FL, recorded the second-highest gain at 18.3%, while Boston ranked third at 10.6%. St. Louis posted the lowest annual rent price gain at 5.2%. While rent growth in many fast-growing metros has decelerated compared to last September, return to offices, colleges and cities is driving rent growth higher in other metros where rent growth was lagging, such as Boston, New York, Chicago, Philadelphia.

According to CoreLogic, the SFR market accounts for half of the rental housing stock, yet unlike the multifamily market, which has many different sources of rent data, there are minimal quality adjusted SFR transaction data. CoreLogic constructed its SFRI for close to 100 metropolitan areas—including 47 metros with four value tiers—and a national composite index. The SFRI analyzes data across four price tiers: Lower-priced, which represent rentals with prices 75% or below the regional median; lower-middle, 75% to 100% of the regional median; higher-middle, 100%-125% of the regional median; and higher-priced, 125% or more above the regional median.

Differences in rent growth by property type emerged after COVID-19 took hold, as renters sought standalone properties in lower-density areas. This trend drove an uptick in rent growth for detached rentals in 2021, while the gains for attached rentals were more moderate during this time.

“As single-family rent prices continued growing at a rapid pace, preferences for attached rentals began to emerge in early 2022, and by summer, had higher increases than detached properties. Attached single-family rental prices grew by 10.7% year over year in September compared to the 9.3% increase for detached rentals,” added Boesel. “However, detached rental price growth is still outpacing that of attached homes on a two-year basis, a respective 22.6% increase compared with 19.6%.”

Read Source Article [www.dsnews.com]